|

Mazano Hub Newsletter Zimbabwe's Diaspora Economy: Remittances Are Becoming the New Venture CapitalOver $2 billion flows into Zimbabwe from its diaspora every year. Most of it is consumed. A quiet shift is beginning to change that. April 3, 2026 | Mazano Hub Weekly |

||||

Every month, Tinashe sends money home. He is a nurse in Manchester. His cousin runs a small hardware store in Harare. The transfer is not an investment. There is no return agreement, no milestone check-in, no structured expectation of growth. It is family keeping family afloat — and across Zimbabwe's diaspora, this is the dominant model of capital transfer.

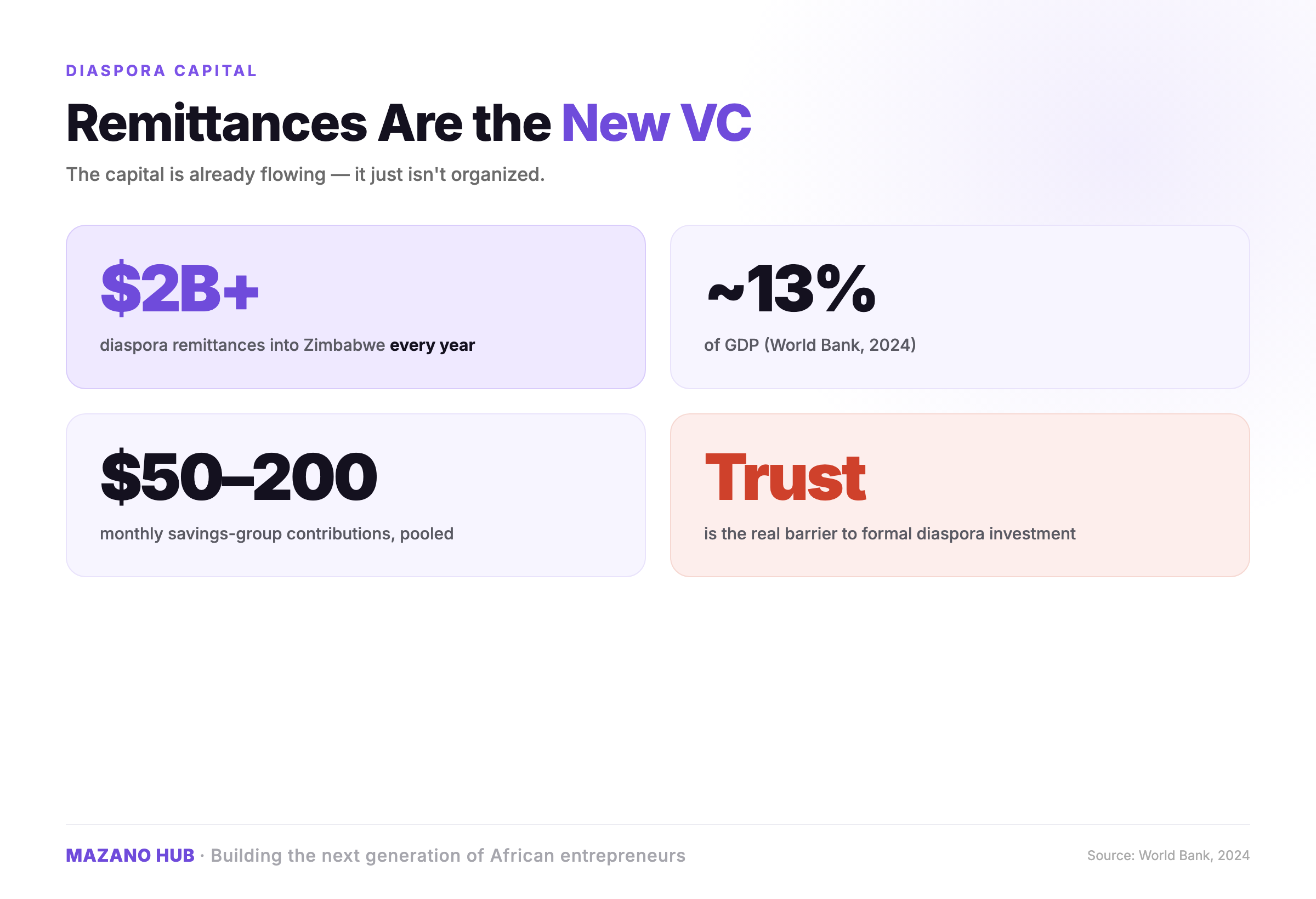

But something is shifting. Slowly, and in ways that institutional finance has yet to fully document, Zimbabwe's diaspora is beginning to treat its capital differently. Giving circles are becoming investment pools. Church fundraisers are seeding businesses. WhatsApp groups are evolving into accountability structures that rival formal due diligence. The line between remittance and venture capital is blurring — and for Zimbabwe's entrepreneurial class, this matters enormously. The Scale of What Is Already FlowingZimbabwe's formal remittance inflows exceeded $2 billion in 2024, according to World Bank estimates — equivalent to roughly 13% of GDP. This figure captures only what moves through licensed money transfer operators. Informal channels — the cash brought in by travellers, the goods shipped in containers, the peer transfers through mobile wallets — push the real number considerably higher. This capital is not neutral. It arrives with social weight. It is expected. It carries obligation. And because it comes with obligation rather than expectation of return, it rarely gets directed toward productive investment. Most of it goes to school fees, rent, medical bills, and food. The survival imperative crowds out the investment horizon. The question is not whether the diaspora has capital to deploy. It demonstrably does. The question is what it would take to redirect even a fraction of that flow toward structured, accountable, enterprise-building investment.

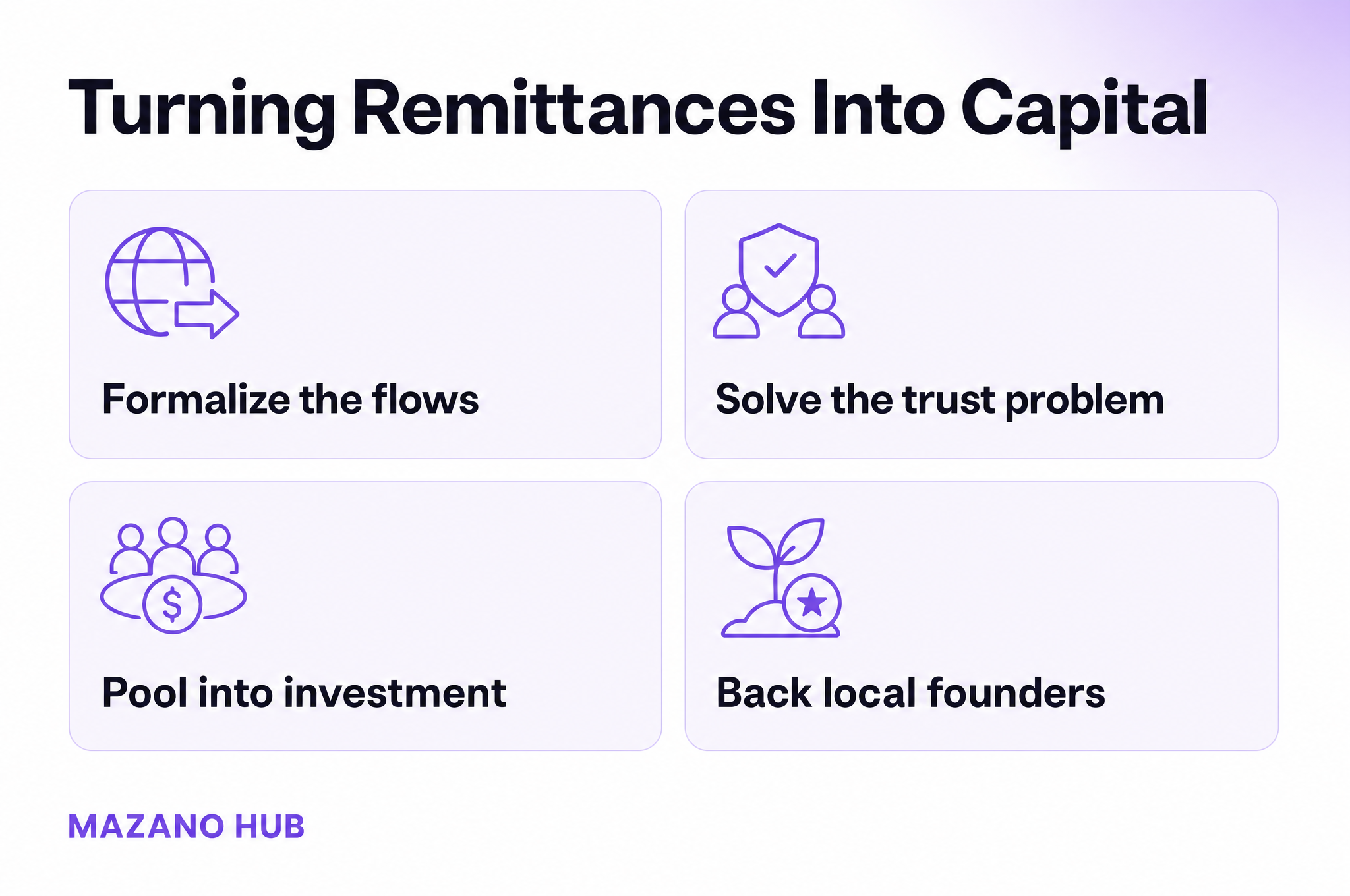

How Diaspora Capital Is Already FormalizingAcross the UK, South Africa, Australia, and North America, Zimbabwean diaspora communities are experimenting with new models. The patterns are recognizable even when the terminology differs. Diaspora Investment Circles Small groups of 8–20 people pooling monthly contributions of $50–$200 each. The pool rotates or is deployed as a collective grant or loan to one member's business idea each quarter. These are informal, trust-based, and effective — but they lack legal structure, due diligence, and any mechanism for learning from failure. Church and Faith-Community Capital Faith institutions in the diaspora — Pentecostal churches, apostolic movements, Catholic development wings — are increasingly being asked to do more than collect tithes. Some are running small business development programs funded by their congregations. Others are acting as trusted intermediaries, verifying home-country entrepreneurs before diaspora donors commit capital. Professional Networks Turning Into Angel Groups A generation of Zimbabwean professionals — engineers, physicians, lawyers, finance workers — has accumulated enough personal capital to begin making strategic investments. Some are doing so individually. Others are organizing into structured angel groups with shared investment theses. This segment is the most sophisticated and has the highest potential to deploy meaningful capital at scale — but it is also the least connected to the early-stage founders who need it most. What all three models share is the same structural gap: there is no trusted, accountable, structured vehicle that connects diaspora capital to validated, mentorship-supported, milestone-tracked founders. That gap is where Mazano operates. The Trust Problem Is the Real ProblemTalk to diaspora investors about why they don't deploy more capital into home-country businesses and the answer is almost always the same: trust. Not distrust of Zimbabwe itself. Not distrust of the ideas. Distrust of the verification layer — the ability to know that a business is real, that a founder is capable, that the money will be used as stated, and that someone will be accountable if it is not. This is not irrational. Zimbabwe's economic history — currency collapses, political instability, the erosion of institutional trust — has created legitimate caution. Diaspora investors have often lost money sent home through informal channels. They have watched well-intentioned family businesses dissolve without explanation. The hesitation to invest is not a failure of love for home. It is a rational response to a broken trust infrastructure.

Building that trust infrastructure is a years-long project. It requires demonstrated track records, transparent reporting, and intermediaries who are credible to both sides — the diaspora investor in Manchester and the founder in Harare. It requires structured accountability systems rather than social obligation alone. It requires, in short, exactly the kind of institution that Zimbabwe's entrepreneurial ecosystem currently lacks. What Mazano Is BuildingMazano Hub exists at exactly this intersection. Our cohort model is designed for founders who are often supported by diaspora networks — people whose startup capital arrives through family transfers rather than institutional grants, whose mentors are in the UK rather than Harare, whose accountability structures are relational rather than contractual. Our Cohort 1 micro-grant pool — launching with applications open July 1, 2026 — is specifically designed to complement diaspora capital rather than replace it. We provide the structured milestone framework, the mentorship layer, and the transparent reporting that diaspora investors need to feel confident. We give founders what they often lack: the accountability infrastructure that turns informal family support into a real foundation for growth. We are also building toward something larger: a diaspora investment vehicle that will allow Zimbabwean professionals abroad to direct capital into Mazano-vetted founders with confidence. This is not a fintech product. It is a trust product — and we are building the track record that makes it credible, one cohort at a time. |

||||

|

|

||||

|

||||

|

You are receiving this because you subscribed to the Mazano Hub newsletter. Unsubscribe · mazano.org · Mazano Hub, Harare, Zimbabwe |